Top three reasons to invest in Jeevan Shiromani = Decent tax-free return + 1 Crore Life & Critical illness cover + Short premium term.

LIC is launching a new money back plan LIC Jeevan Shiromani Plan 847 on 19th December 2017.AssuredGain’s expert reviewns of LIC Jeevan Shiromani Plan 847.

It is a non-linked, with profits, limited premium payment money back plan. LIC has designed especially to target the HNIs (High Networth Individuals). This plan also provides you critical illness cover also.

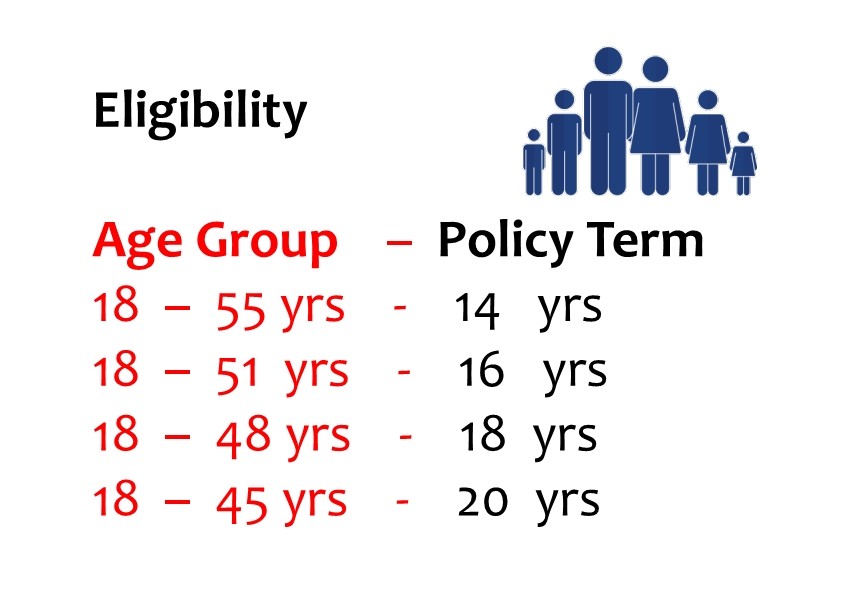

Eligibility of LIC Jeevan Shiromani Plan 847

First, let us see the eligibility condition of LIC Jeevan Shiromani Plan 847.

As LIC is claiming, the minimum sum assured under this plan is Rs.1 Crore. Hence, this is not meant for any ordinary earning individual.

Features of LIC Jeevan Shiromani Plan 847

Along with above-said eligibility conditions, this plan offers the below features.

Benefits of LIC Jeevan Shiromani Plan 847

Now let us see the benefits available under LIC Jeevan Shiromani Plan 847.

This plan offers the guaranteed addition. For the first 5 years, the guaranteed addition will be Rs.50 per Rs.1,000 Sum Assured.

From 6th year onward to till policy maturity, this plan offers the guaranteed addition of Rs.55 per Rs.1,000 Sum Assured.

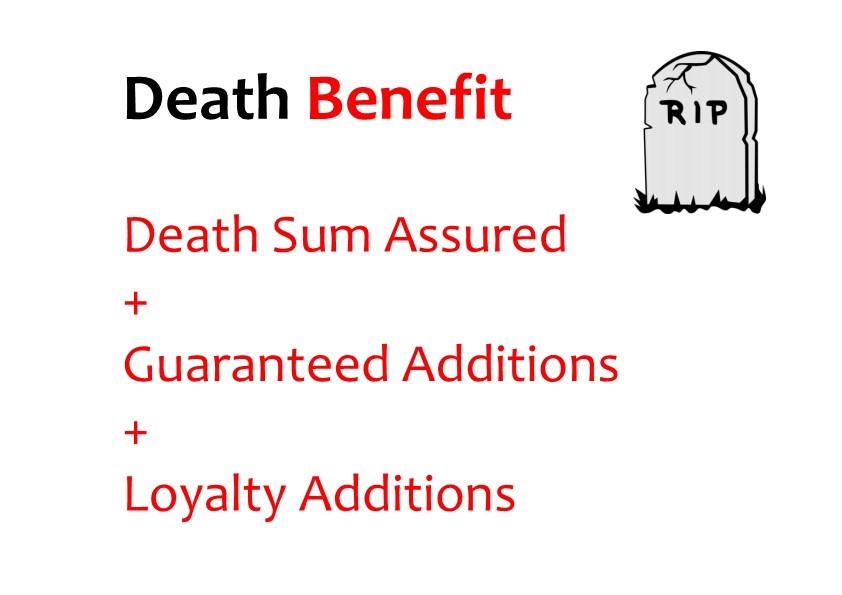

There are two conditions to pay the death benefits under this plan and they are as below.

If death occurs during the first 5 years of the policy period, then the benefit is as below.

Sum Assured on death+Guaranteed Addition at Rs.50 per Rs.1,000 Sum Assured.

Sum Assured on death+Guaranteed Addition (for first 5 years Guaranteed Addition will be at Rs.50 per Rs.1,000 Sum Assured and from 6th year onward it will be Rs.55 per Rs.1,000 Sum Assured)+Loyalty Addition.

Meaning of “Sum Assured on Death” is defined as HIGHER of the below.

You can also defer the death benefits payable to your nominee in installments rather than a lump sum payment is chosen over the period of 5 yrs, 10 yrs or 15 yrs. This can be exercised by the policyholder during his lifetime only. Based on this, the nominee will receive the death benefits at a deferred period set by the policyholder. Nominee can’t alter this feature. This can be either % of the death benefit or absolute value of money.

If policyholder survives to each of the specified duration during the policy term, a fixed % of Basic Sum Assured will be payable. This fixed % is as below.

Like death benefit deferred benefit, this policy offers you to take the survival benefit at the deferred date (postponing the payment receivable). You can receive the survival benefit as per your with along with interest at a later stage of your requirement.

However, you have to defer this survival benefit up to policy maturity only. Before that, you have to receive this benefit along with interest. If you do not take this deferred survival benefit and interest before maturity, death or surrender, then LIC will pay this during maturity, death or surrender time along with interest.

The interest will be yearly compounding but the rate will be fixed by LIC from time to time.

You have to inform this deferred survival benefit receiving option 6 months prior to the actual due date of survival benefit. Otherwise, LIC will pay you the surival benefits as per the due dates.

If policyholder survives up to the policy period, then he will receive the below benefits.

Let me explain the same of both survival benefits and maturity benefits in below sheet for your simple understanding.

Survival and Maturity Benefits under LIC Jeevan Shiromani Plan 847

Hope the benefits of LIC Jeevan Shiromani Plan 847 may be understood you now easily.

In this plan, you can defer your maturity benefit for future dates in installments. The periods available is for 5 years, 10 years or 15 years. This option can be exercised by policyholder only.

You can choose either % of net maturity amount or absolute value to be payable in installment for the next 5 years, 10 years or 15 years. LIC will pay you in advance of such installments. The installments available are yearly, half-yearly, quarterly or monthly.

The applicable interest on this installment will be declared by LIC from time to time.

The policyholder has to inform LIC 3 months prior to maturity date about this option. During such deferred maturity benefit period, if policyholder wishes to discontinue and interested to commute the remaining installments as a lump sum, then he can opt that.

If the policyholder dies during such deferred maturity benefit period, then the remaining installments will be payable to the nominee. The nominee has no rights to alter this deferred benefit installment option.

Along with the above-shared death, survival and maturity benefits, this plan also offers the inbuilt critical illness benefits.

On the first diagnosis of any one of the 15 Critical Illness as specified below, and also if the policy is in force, then the following benefits will be provided.

But before that let us first understand of what are those 15 critical illness which this plan covers. They are as below.

Once you are diagnosed with an above-said illness, then LIC will give you the below benefits.

Inbuilt critical illness benefits equal to 10% of Basic Sum Assured will be payable subject to the following.

If LIC accepted the critical illness claim, then you no need to pay the premiums for the next two years. LIC will not charge any interest on such delayed payment. However, if there is a survival benefit dues to be payable to policyholder during this 2 years period, then LIC will pay the survival benefit by DEDUCTING the premiums due.

Under this benefit, the policyholder has an option to take the second opinion from the LIC empaneled healthcare providers or through reputed hospitals in India based on the arrangement made by LIC.

Do remember that this facility is available only once during the policy period, for which you no need to pay the cost. The policyholder can take this second opinion immediately after informing LIC about the illness (without bothering about whether his critical illness benefit will be accepted or not).

However, such second opinion not involves any test. If you do the test, then you have to bear the cost of that.

Also, such second opinion is purely based on the facilities and recommendations LIC provide.

Let me explain the benefit illustration with below image.

Benefit illustration of LIC Jeevan Shiromani Plan 847

What returns we can expect from LIC Jeevan Shiromani Plan 847?

Let us consider that Mr.X whose age is 30 years opted for Rs.1 Cr LIC Jeevan Shiromani Plan 847 and term of the policy is 20 years, then we can expect the returns as below.

Returns from LIC Jeevan Shiromani Plan 847

You notice that Mr.X will pay the premium up to 16 years only. However, he receives the survival benefit of Rs.45 Lakh on 16th year and 18th year. On maturity, he will receive remaining 10% of Sum Assured+GA+LA.

I considered the LA rate as Rs.200 per Rs.1,000 Sum Assured. Few may argue that this too less by comparing other plans which NOT offers you guaranteed addition. If you check the LA rate of Jeevan Shree (which offers GA like this plan) with the LA rates of other plans, then you notice that LA rate of Jeevan Shree is too less than other plans.

Hence, considering this trend of LIC, I considered the fair value of Rs.200 as LA for calculation. You notice that return on this investment is just around 6%.

Review of LIC Jeevan Shiromani Plan 847

# This plan is not for all. Because the minimum sum assured under this plan is Rs.1 Cr. Hence, if you afford around Rs.5 lakh to Rs.10 Lakh premium then you can opt for this plan.

# The new feature of this plan is eligiblilty for paid up, surrender and loan immediately after one-year completion of the policy period. Usually, LIC plans eligible for paid up and surrender after 3 years. However, LIC reduced this to one year for this plan. In our view, LIC reduced this to one year to make sure that LIQUIDITY must not be an issue.

# This plan offers an inbuilt critical illness cover. However, do remember that getting a claim from critical illness is not so easy and hence you must understand the pros and cons of such critical illness rider benefits. Only 15 illness are covered under this plan.

# If death occurs within 5 years of the policy period, then your nominee will receive SA+GA @ Rs.50 per Rs.1,000 SA. However, if death occurs after 5th year to policy period, then your nominee will receive SA+GA @ Rs.55 per Rs.1,000 SA. Hence, the probability of your nominee receive during the first 5 years is less.

# LIC now started to offer to defer the survival benefit, death benefit and maturity benefits to its plans. However, choosing such options blindly without knowing the interest rate offered by LIC is like a BIGEST mistake. Because, if death occurs, then-nominee has no rights to change these options. The nominee has to continue with the option which policyholder selected. Hence, be careful while exercising this option.

# Coming to returns part, you noticed from above illustration that this policy will give you around 5% to 6% returns. Hence, in no way it is even beat the current inflation rate. Hence, it is waste if you invest for such a long period but get a return which around 5% to 6% tax-free return which is quite good when bank offers same return with taxation.

Conclusion:-This is the best plan forHNIs (setting minimum sum assured as Rs.1 Cr), deferring your survival, death and maturity benefits, inbuilt critical illness rider and eligibility for paid up and surrender within a year.

Introduction to a Transformative Career Opportunity The Life Insurance Corporation of India (LIC) has pioneered…

In today’s fast-paced financial world, securing your financial future requires more than just saving money—it…

Introduction Special needs financial planning involves preparing for unique challenges, whether it's supporting a child…

Shriram Life Assured Avoid this plan with low returns! Looking for a reliable way to…

Doctors are the pillars of our healthcare system, dedicating their lives to the well-being of…

Retire Stupid! When it comes to retirement planning, insurance companies often market their unit-linked insurance…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}